")

Stocks were hit hard from Friday to Tuesday with the S&P 500 SPDR, Nasdaq 100 ETF and others recording outsized declines. Today we start with these outsized declines and show what they entail going forward. Stocks were already extended and these sharp declines signal the start of a corrective period. At this point, I will treat any weakness in SPY and QQQ as a correction within a bigger uptrend.

The S&P 500 SPDR (SPY) fell over 2% this week for the biggest weekly decline since June. The long-term trend is still up because SPY remains well above the rising 40-week SMA. However, a big Spinning Top candlestick formed last week and a volatility indicator ticked higher. Spinning Tops signal indecision that

SPY: You Spin Me Right Round Read More »

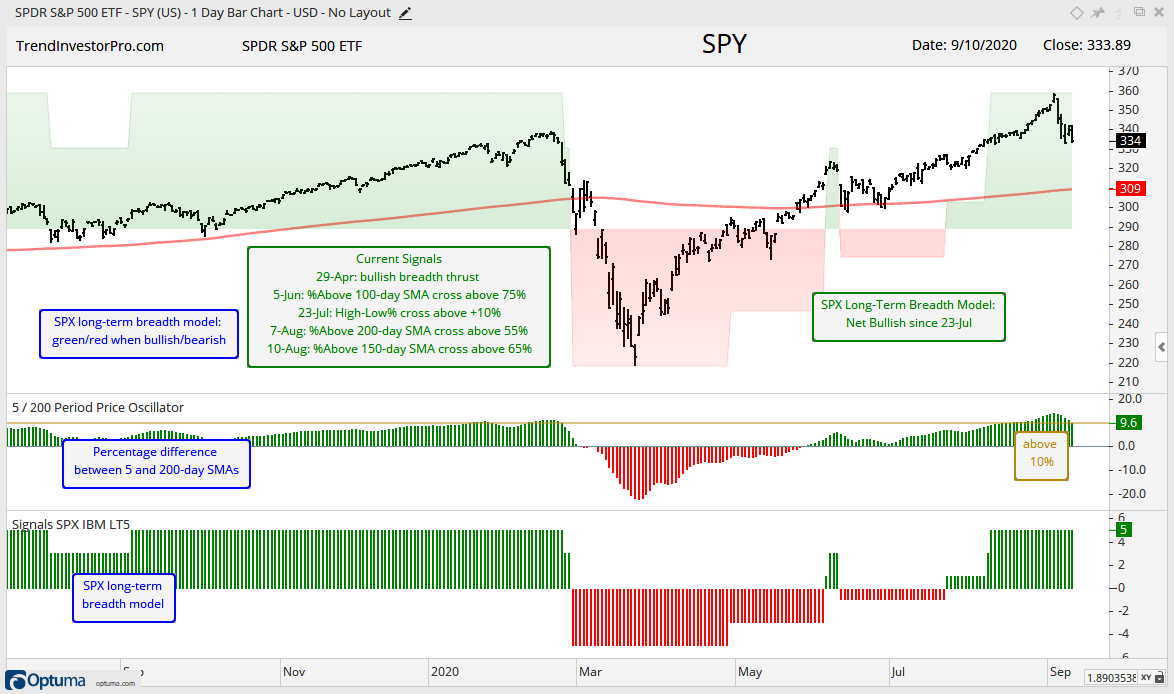

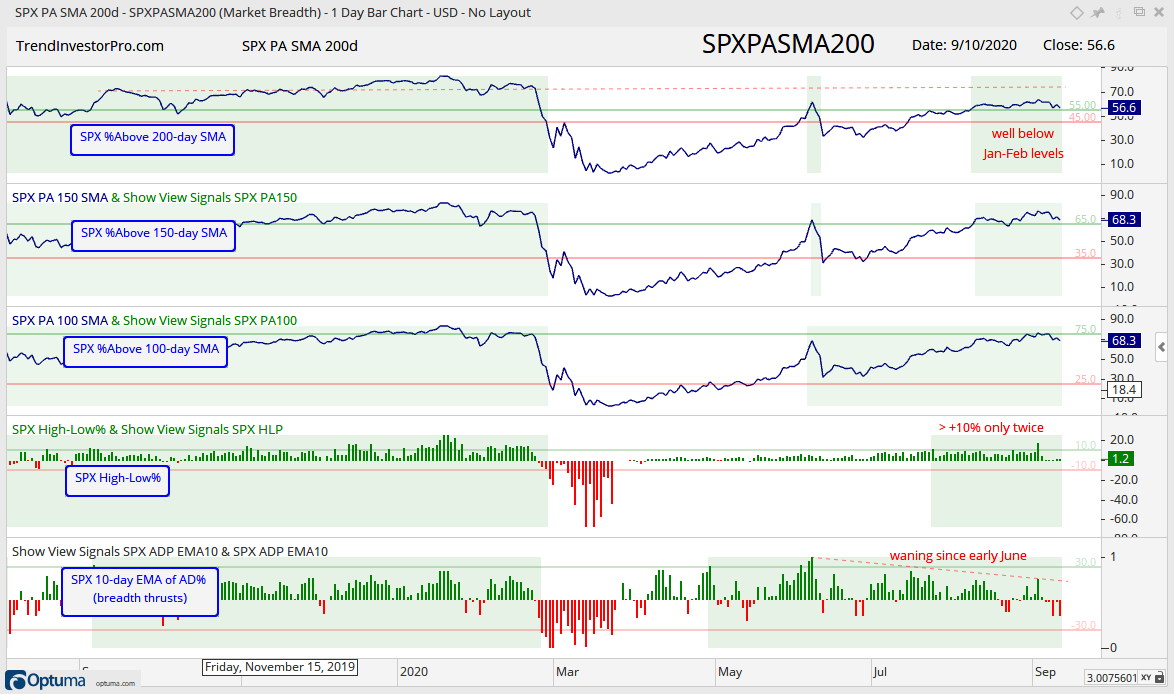

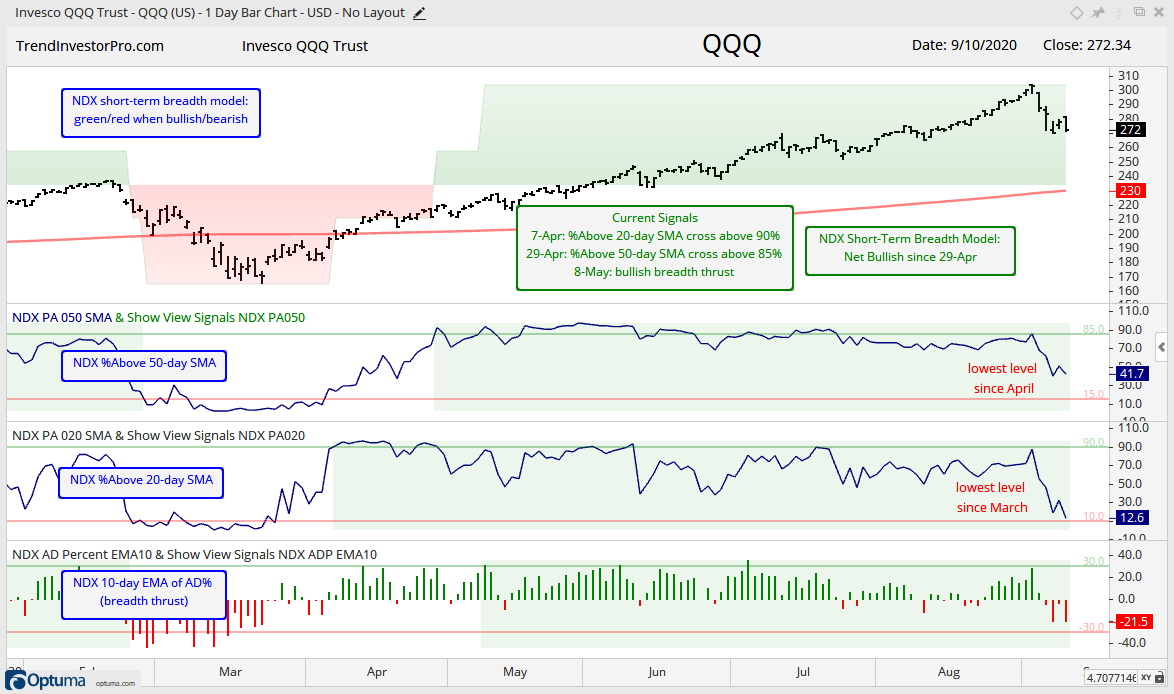

The extended uptrend in stocks hit a speed bump this week with a sharp decline on Thursday-Friday. Today we will review the percent above 200-day SMA indicators and their extended nature. Attention then turns to the medium-term indicators, which turned mixed this week. The odds for a correction were already brewing and it looks like some sort of correction is unfolding. I will look at potential targets for SPY and QQQ, as well as for several ETFs in the ChartBook. Elsewhere

The bears fired a shot across the bow, but one or two days is not enough to reverse a strong uptrend. There were already warnings of a correction or pullback because SPY has been more than 10% above its 200-day since August 12th and QQQ has been 20% above its 200-day since July 6th. Of course, overbought indicators are not very good for timing a correction. In fact, I have yet to find a good indicator for timing a peak/pullback during a strong uptrend.

Overextended its an incredibly nebulous term. Many ETFs were considered overextended last week and simply became even more so as strong buying pressure persisted. This is a classic case of becoming overbought and remaining overbought because the uptrend is strong. These ETFs, which are in the first few groups, are in the trend-monitoring phase.

Verizon (VZ) participated in the first leg up from late March to mid April, but then stumbled with a decline into mid June. This stumble, however, looks like a classic correction and the stock broke out with a strong move over the last six weeks. In addition, the TIP Trend Composite, which aggregates five trend-following indicators turned positive in early August. Let’s investigate further.

Trend Composite Turns Fully Bullish for Verizon Read More »

Today’s video starts with an overview of the breadth models for the S&P 500, Nasdaq 100, Mid-caps and Small-caps. We then turn to the all important medium-term trend and the four key indicators to watch. Diving into the chartbook, there are flag breakouts working in IWM and XLI. REITs are perking up and making good on their Bollinger Band breakouts. The gold and silver ETFs have bullish patterns and mean-reversion setups in the making. Bond ETFs, however, extended their pullbacks after the Fed announcement. The video finishes with

We all know that the S&P 500 is driven by large-caps, especially the big four, which account for over 20% of the index (AAPL, MSFT, AMZN, GOOGL). Furthermore, most of us are aware that breadth measures are not as strong as the S&P 500 and this is reflected in the S&P 500 EW ETF (RSP), which has yet to clear its June high. Breadth, however, is not exactly weak. It is just strong enough to sustain the advance. In other words, the cup is half full, not half empty.

Stock-related ETFs remained strong and many so-called overbought ETFs became even more overbought as their uptrends extended. Many ETFs are in the trend-monitoring or waiting phase. The early breakouts occurred in July and these ETFs followed through with further gains the last several weeks. Some tech-related ETFs stalled in late July and early August, but caught a second wind with breakouts over the last few weeks.

The total number of new highs in the S&P 500, S&P MidCap 400 and S&P SmallCap 600 continues to underwhelm. Even so, new highs are still outpacing new lows and this is enough to keep the uptrend since late March going. The first chart shows new highs and lows for the three indexes with horizontal lines at the 10% level (e. g. 50 and -50 for the S&P 500).

New 52-week Highs Underwhelm, But Outpace New Lows Read More »

The bulk of the evidence remains bullish for large-caps, large-cap techs and mid-caps, but mixed for small-caps. I am also seeing mixed performance within the S&P 500, especially when looking at the equal-weight sectors. Technology, Healthcare and Consumer Discretionary remain strong, while Finance, Energy and REITs are weak. Finance is the only big sector that shows underlying weakness though.

Today’s video will focus on the core ETF charts. We will start with the scatter plot and see that the bond ETFs in the upper left, which means they are oversold and in uptrends. On the ranking tables, ETFs related to Consumer Discretionary, Healthcare and Technology are leading. I continue to follow the Chandelier Exits for several ETFs as their uptrends extend (XLY, ITB, XRT). Elsewhere

Despite the usual pockets of weakness, there is still plenty of strength out there in ETF land. Housing, Retail and Consumer Discretionary ETFs moved to new highs. Tech-related ETFs remain mixed with some hitting new highs and some moving back into their consolidation patterns. Precious metals ETFs got sizable mean-reversion bounces, but it looks like volatility is picking up in this group.

I received some pertinent questions over the weekend and create a post to share the answers. My email answers were not as detailed as in this post, which provides more details and examples. The first question deals with the StochClose ranking and how to use it. This answer will also highlight seven broad trading strategy groups. Second

Today’s video starts with a long-term weekly chart of the S&P 500 SPDR and the reason I consider this advance as a medium-term uptrend. The medium-term trend indicators remain in bull mode and the mid-cap breadth model turned bullish this week as participation broadened. We can see this in the ranking tables as the StochClose values shot up for the Industrials SPDR and Regional Bank ETF.

Weekend Video – Participation Broadens as Mid-caps, Industrials and Banks Perk Up Read More »

Even though the current advance is getting quite extended, the broad market environment remains bullish and the medium-term uptrends rule. Tech-related ETFs and stocks drove the market higher from late March to late June. Even though the tech surge slowed, participation broadened over the last six weeks as other groups picked up the slack. The Industrials SPDR (XLI) is the top performing sector since July 1st

There are still a lot of uptrends out there in ETF land, and this includes some key stock-related ETFs. Nevertheless, we are seeing some rotation at work the last few weeks. The tech-related ETFs slowed their advance and some even failed to hold their breakouts. Meanwhile, ETFs related to consumer discretionary continued higher and are leading the pack. However, some of these new leaders are getting extended (XLY, XHB).

Today’s video starts with the medium-term indicators and the overall trends for the S&P 500 SPDR, S&P 500 EW ETF, S&P MidCap 400 SPDR and Russell 2000 ETF. These are the broadest index ETFs out there and money moved into mid-caps and small-caps this week. The advance since April is marked by falling volatility and we will look at two indicators to monitor volatility.

The Healthcare SPDR (XLV) is one of the strongest sectors in 2020. Even though it does not sport the biggest gain, XLV recorded a new high in July and some 80% of its components are above their 200-day EMAs. The new high points to a long-term uptrend and upside leadership, while the percentage of stocks above the 200-day EMA points to broad strength within the sector. Sector SPDRs, however, are only as strong as the sum of their parts (component stocks).

Four Stocks Poised to Drive Healthcare Higher Read More »

The chart below shows year-to-date performance for the top 20 stocks in the S&P 500. Overall, the year is mixed with eleven up and nine down. Amazon is up over 70%, Apple is up over 50% and Microsoft is up over 30%. Facebook and Home Depot are dragging their feet with gains greater than 20%. As strong as the stock market seems, strength is clearly concentrated in a few stocks. Moreover, these few stocks are up big, really big.