")

There are plenty of ETFs with corrections or downtrends the last few months, but some of these are showing short-term relative strength. Similarly, several tech-related ETFs firmed with hamari on Monday-Tuesday and closed strong on Wednesday.

Large-caps finally pulled back with the S&P 500 SPDR falling around 5% in September. Small-caps held up better with a smaller decline. Overall, there was a rotation underway in September as money moved into banks, energy, airlines and defense.

The streak finally ended as the S&P 500 fell more than 5%. Using SPY as the proxy, the ETF had gone some 227 days without a pullback of more than 5% (closing prices). The 5.31% decline here in September is the largest since October 2020. SPY fell around 10% in September

There are some new trend signals over the last five days. The Bank SPDR (KBE) and Regional Bank ETF (KRE) followed through on last week’s surges and StochClose moved above 60 to turn bullish. Also notice that the 52wk Range

Signs of a market rotation began to appear last week as the 10-yr Treasury Yield surged, the 20+ Yr Treasury Bond ETF plunged and the Regional Bank ETF advanced over 3%. Techs and high-flyers held up relatively well last week, but got pummeled on Tuesday with many falling more than 3%.

As its name implies, the Zweig Breadth Thrust quantifies bullish breadth thrusts using a setup level and a signal level. The setup occurs when the 10-day EMA of Advances / (Advances + Declines) dips below .40 and the bullish signal triggers

Zweig Breadth Thrust Hits Lowest Level since May – What Does it Mean? (Premium) Read More »

Stocks were hit hard on Monday-Tuesday with dozens of ETFs becoming oversold, including SPY. These oversold conditions gave way to a strong rebound the rest of the week with Finance and Energy leading the way. Bonds threw a small tantrum after the Fed meeting as the

The Fed has yet to actually start tapering, but dropped some hints that it would if the economy continues to strengthen. The bond market, which tends to lead the Fed, reacted violently as the 20+ Yr Treasury Bond ETF fell over 2% and the 10-yr Treasury Yield broke above

After a dozen new uptrend signals in late August and early September, the tide changed as the S&P 500 experienced its first 4-5 percent pullback since May. This pullback was enough to reverse some of the new uptrend signals and there were 14 new downtrend signals over the last five days. I am referring only to the 113 equity-related ETFs

The Market Regime remains bullish and the S&P 500 is just 4% below its recent high, but breadth has been waning for months and many groups are already in corrective mode. The 4% decline

The market regime remains bullish, but breadth continues to wane and more breakouts are failing. Overall, ETFs related to tech, healthcare, communication services and REITs are leading, while ETFs related to industrials, materials and housing are lagging because their breakouts failed to hold. I am also watching TLT and the Dollar because

The stock market remains in a funk. Large-caps finally pulled back with the S&P 500 loosing a whopping 2% from high to low (Sept 2 to 14). SPY remains is a clear uptrend with a rising channel and QQQ has not touched its 50-day SMA since June 3rd. Things are different outside of the S&P 500 because

The broad market environment remains bullish for stocks and the vast majority of equity related ETFs are in uptrends (bullish StochClose signals). Even so, I remain concerned with the broader market environment because breadth continues to deteriorate and a number of ETFs peaked months ago. The Russell 2000

The S&P 500 SPDR (SPY) fell five days in a row for the first time since October 2020, scene of the last decent correction in the stock market. Signs of a correction continue to build as breadth wanes and key metrics hit their lowest levels since last year. We are also seeing corrections or downtrends

The list of ETFs with uptrend signals over the last three weeks reads line the who’s who of the high flyers. This list includes the Video Games eSports ETF (ESPO), the ARK Innovation ETF (ARKK), the Clean Energy ETF (QCLN)

Trend-Signals: Take Right Away or Wait for a Pullback? (Premium) Read More »

Timing a correction in the S&P 500 has been a fool’s errand since the November surge and breakout. The index brushed off negative seasonality in February and August. Techs and high flyers declined from mid February to mid May, but the S&P 500 kept right on trucking as money rotated

Of the 113 ETFs in the Core List, 79 are in uptrends (70%) and 34 are in downtrends (30%). This is more than enough to support a bull market in stocks. Six of the seven major index ETFs are in uptrends (SPY, RSP, MDY, IJR, IWM , QQQ) and one

SPY continues on its stairway to higher prices with another new high this week. We are also seeing strength in mid-caps as MDY holds its breakout and new trend signals in small-caps (IJR and IWM). Breadth is not as strong as it used to be, but strong enough to support a bull market. Yield spreads show no signs of stress and the

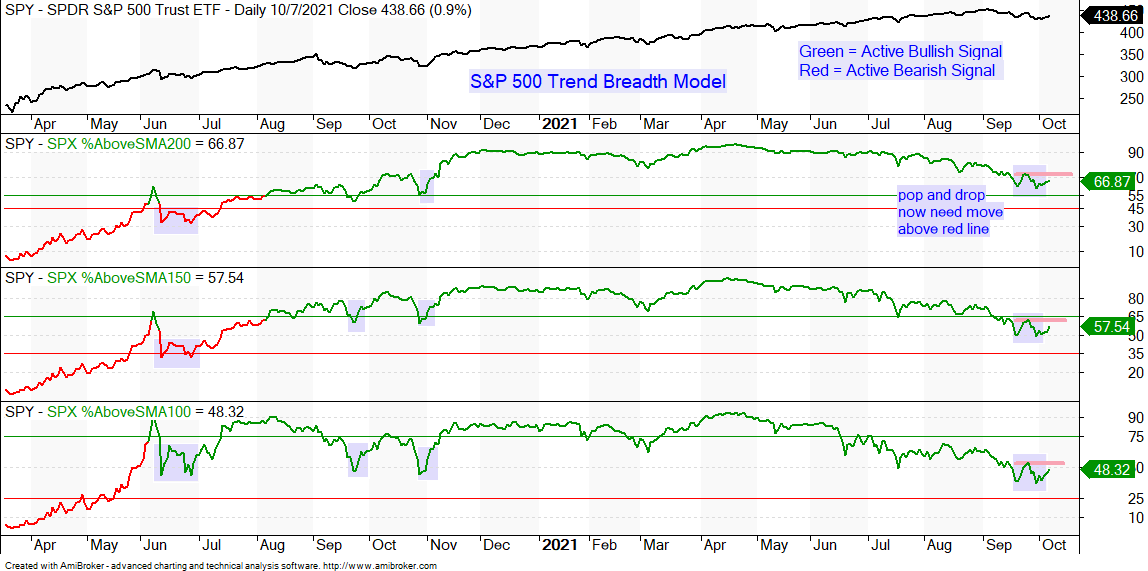

Breadth remains bullish overall. Some 80% of S&P 500 stocks are above their 200-day SMAs and High-Low Percent expanded to

There were several new uptrend signals this past week and these signals suggest a stronger risk appetite in the stock market. Today’s report will review the StochClose indicator and some of these new trend-following signals. We will also show these signals on the revamped Ranking and Trend Table. Today’s charts also